Seize the day: B2B2X as a unique growth opportunity for the entire financial ecosystem

What is B2B2X, why is it a compelling concept, and how can the regulators, the incumbents, and the disruptors capitalize on this new growth engine for the digital age?

With many incumbent financial services providers showing sluggish revenue growth, and with the diminishing value of the FinTechs who were meant to disrupt them, it’s only logical to wonder where the future growth in the industry may come from. And yet – as ever – these negative pressures are breeding new, innovative ways of collaboration between seemingly opposed segments of the financial services (FS) industry. Furthermore, the industry regulators are increasingly pointing to systemic issues that can only be resolved by collaboration across the FS ecosystem.

Just like big business is re-focusing on unlocking the growth potential within the small and medium business segment (B2b), so the incumbent FS providers and innovative FinTechs are increasingly embracing each other in a new iteration of an old concept captioned in a fancy acronym – B2B2X.

B2B2X – the incumbents and the disruptors come together for the win

In broad strokes, B2B2X (comprising of B2B2B and B2B2C) entails businesses enabling other businesses to better serve their customers, whether consumers or other businesses. Global Banking and Finance Review calls this “the go-to business model for startups and FinTechs”, and it is easy to see why. To understand the appeal of B2B2X, it’s important to look at it as a concept born out of necessity, which neatly solves the growth issues faced by the incumbents and the disruptors alike. B2B2X jointly builds on their respective strengths – and makes up for their weaknesses – to the point where everybody in the value chain wins.

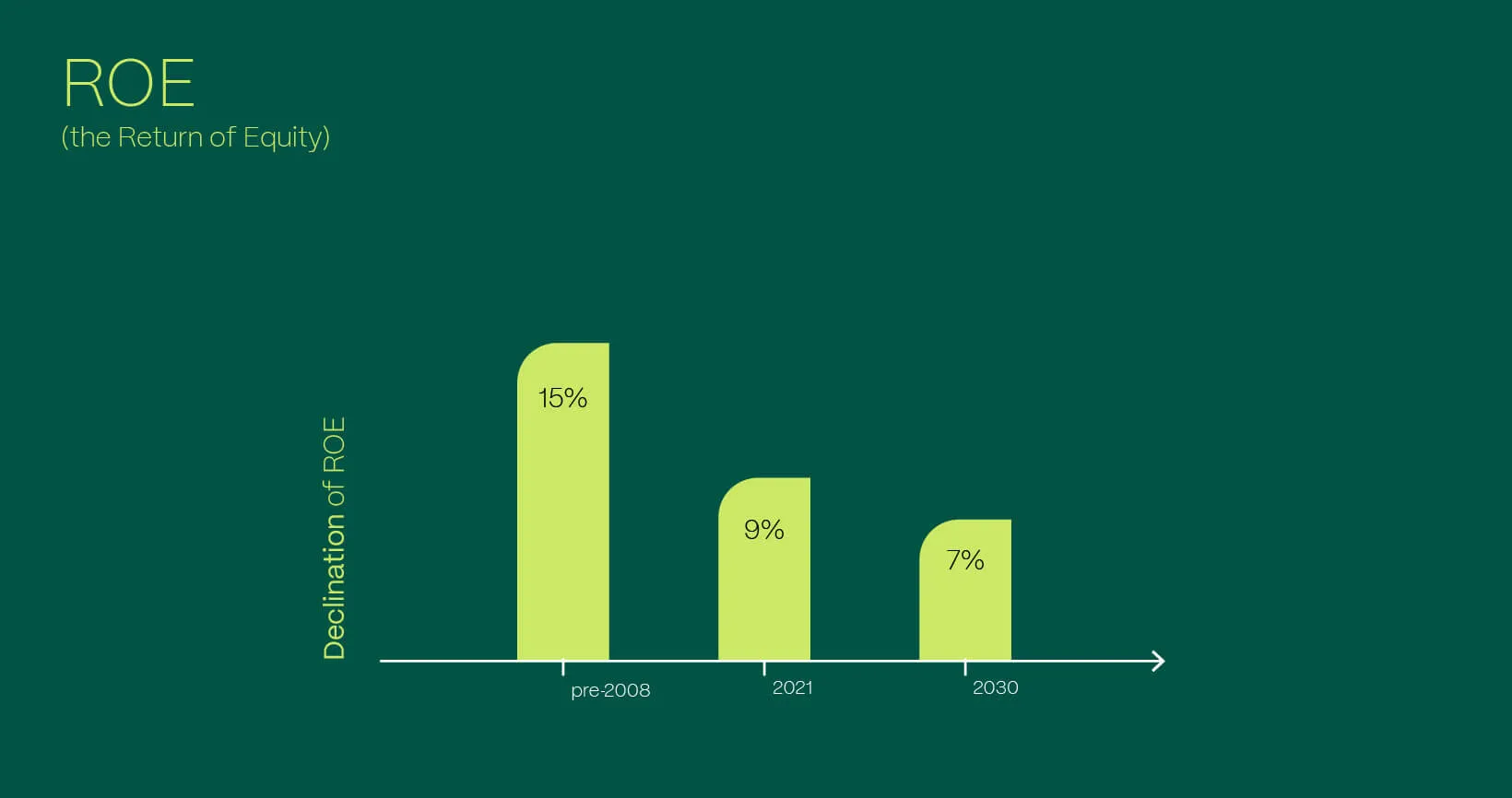

According to the McKinsey report mentioned above, the Return on Equity for traditional banks has declined to 9% in 2021, compared to 15% pre-2008. This decline is expected to continue to about 7% by 2030 – a concerning, long-term trend. This stagnation can largely be ascribed to tech advances having brought into question size as an advantage in providing excellent, innovative services. Large organizations are stable, yet the same processes and ways of doing business that make them stable also render them slow to innovate.

FinTechs, on the other hand, are small, nimble, and agile – and therefore breed the very innovation that brings the traditional incumbent providers’ future growth into question. And yet, FinTechs lack the very scale and financial stability that renders the incumbents so slow to innovate, but also gives them market leverage. While some FinTechs have typically addressed this challenge with the support of truly impressive levels of funding, their sources of funding are starting to dry up. In Canada, my own home market, FinTech investment “was reduced to less than half in the first six months of 2023 from last year”, according to KPMG. High interest rates and shrinking risk appetites make this a global phenomenon.

You can now start to see the appeal of B2B2X. The incumbent FS players can lean on FinTechs to leverage their innovation, which enables superior service to the market and re-fuel increasingly stagnant industry growth. By the same token, rather than having to compete with the massive capital and influence of the incumbents, FinTechs can benefit from the incumbents’ investment. It's a win-win!

Three compelling ways to capitalize on the B2B2X concept

Having established the viability of the concept, I’d like to turn to three practical models it can be applied to as you look to capitalize on B2B2X as a future growth driver:

- embedded finance;

- value chain disruption;

- infrastructure-as-a-service (IAAS).

Embedded finance – how specialized FinTechs can tap into the broader market

Embedded finance is already all around us – whether we’re offered insurance when buying a new TV, or we’re offered installment payments to finance the said purchase. And yet, I am convinced that this barely scratches the surface of the overall potential. Embedded finance offers the opportunity for innovative yet specialized FinTechs to become an essential part of a tremendously large market.

Let’s say you’re a FinTech specializing in customer authentication. Your innovative model to enable retinal scans cost-effectively on a large scale – to use but one example – could potentially be embedded into every large transaction globally as the incumbents look for secure ways to enable an ever higher volume of high-value transactions.

Or, you may be a startup innovating the intersection of Artificial Intelligence and data analytics. Use cases are many – your product could be used to identify fraudulent transactions before any current method could achieve this, or your analytics suite may be offered as a value add to a payment solution offered to small and medium enterprises such as small retailers. Indeed, this second use case presents an exciting convergence of the B2b and B2B2X concepts.

In the past, specialization and lack of scale were a disadvantage that prevented startups from reaching a broader market. These days, thanks to the resurgence of B2B2X, this specialization is precisely what an incumbent may seek in a FinTech partner in order to advance their value proposition.

B2B2X value chain disruption enables exponential growth in a time of crisis

Speaking of evolving value propositions, B2B2X naturally lends itself to value chain disruption – and nowhere is this more obvious than in the financial services industry.

I’ve referenced above the stagnating revenues among the large FS institutions. In the UK, EY expects mortgage lending to grow by a mere 0.4% by the end of 2023. In the US, Sam Kather, the Chief Economist at Freddy Mac, likewise expects “greater stagnation in the housing market… pushing demand and home prices further downward.” It is easy to see how quality lead generation will make or break traditional mortgage providers. It is in this bleak economic picture and against the backdrop of blurring lines between the digital and the physical realms that innovative FinTechs can embed themselves between the mortgage providers and the consumers. Under this model, they can now leverage advanced algorithms and AdTech to provide high-quality leads to mortgage providers.

Similarly, climate risk is becoming an emerging issue that wasn’t a consideration just a decade or two ago, and this presents a great opportunity. Insurers and lenders alike will be looking for highly specialized models to ensure their customers are properly evaluated and protected against the backdrop of increasingly unpredictable climate risks. Indeed, these will increasingly become a regulatory requirement. Whether you’re a FinTech with an advanced climate risk assessment and valuation model, or provide value-added climate risk intelligence that the incumbents can offer to their clientele – the market opportunity is ripe.

Crisis begets innovation, which is in turn, a key ingredient in value chain disruption. As McKinsey points out, “both individual and organizational customers now seek a long list of attributes from their financial service providers”. B2B2X offers FinTechs an unprecedented opportunity to embed themselves in value chains that were previously hermetically sealed and impervious to change!

Infrastructure-as-a-service – FinTechs are becoming indispensable to the incumbents’ success

Is there a more impressive case of value chain disruption than Amazon Web Services (AWS)? Amazon, originally an eCommerce book retailer, now generates 74% of its operating profit from AWS! Web service infrastructure is an indispensable enabler to virtually any business these days, and this model offers a clue as to how FinTechs can leverage the B2B2X model to become indispensable players across different markets – by providing infrastructure-as-a-service.

The specialized infrastructure needs of the incumbent FS providers in the new digital frontier are near-endless. Think cybersecurity, data analytics, KYC requirements, UX, lead generation, underwriting… Each of these needs presents a viable point of entry into a long-term infrastructure play for a challenger tech provider.

Take cybersecurity as an example. The Fed has acknowledged the obvious very clearly: “Cyber risk in the financial system has grown over time as the system has become more digitized, as evidenced by the increase in cyber incidents”. Every statement from the Fed – as obvious as it may seem – reverberates loudly in the market. As regulators increasingly focus on cyber risk requirements for the established financial players, the costs of meeting those regulatory requirements grow. Imagine becoming the provider of choice of cost-effective and efficient cyber security infrastructure to the financial services ecosystem.

The larger the ecosystem an organization enables in the B2B2X model, the more significant the revenue potential. Providing infrastructure – though – also ensures the long-term stability of said revenue source. This is truly an ideal scenario that demonstrates the viability of the B2B2X concept.

All parties must seize the unique moment to capitalize on B2B2X as a growth lever

B2B2X, as seen in the above example, represents a unique coming together of the incumbents, the FinTech disruptors, and the financial industry regulators. And this coming together is not without risks. Success in this scenario can provide dream returns, and yet failure can have catastrophic reputational, regulatory, and even macroeconomic consequences.

What is needed to make this scenario a success is coordination between all three sides in seizing the unique moment of opportunity provided by B2B2X and the current economic situation? Regulators ought to provide an environment that leads to the development of a transparent, safe, and collaborative financial ecosystem by rewarding such behaviors from the key players, and by discouraging their opposites. The incumbents need to be open-minded and accept innovative FinTechs as the enablers and enhancers of their traditional business models to the benefit of their customers – whether individual or corporate. And FinTechs should be putting their best foot forward to demonstrate to the incumbents and regulators alike that their offering is not a fleeting, risky trend – but an indispensable component of future growth and market participant satisfaction.

At Vega IT, we have extensive experience working with both the incumbent FIs and FinTechs. This means we can help FIs leverage FinTech solutions to deliver innovative products to their customers, and we can help FinTechs to develop industry-grade solutions with strong value propositions for the incumbent FIs.