The new economics of insurance in the era of AI

Artificial intelligence has become a structural investment in insurance, not a technology experiment. The insurers that redesign their operating models around AI are gaining a lasting advantage and setting the pace for the industry.

Artificial intelligence has become one of the most significant investment priorities in insurance because the economics of the industry have moved beyond what legacy operating models can support. Research consistently shows that underwriting, claims, fraud detection, and customer operations are evolving faster than traditional processes can handle.

Yet most insurers struggle to scale AI, limited by fragmented data, outdated systems, and governance models built for a different era.

The divide is pretty clear. Using AI as a tool creates incremental gains. Redesigning the operating model around it creates a structural advantage.

Where investment is actually flowing

Insurers are directing capital towards areas where data availability is high, operational friction is significant, and financial outcomes are measurable.

Five domains consistently dominate AI investment across global markets.

1. Claims automation and straight-through processing

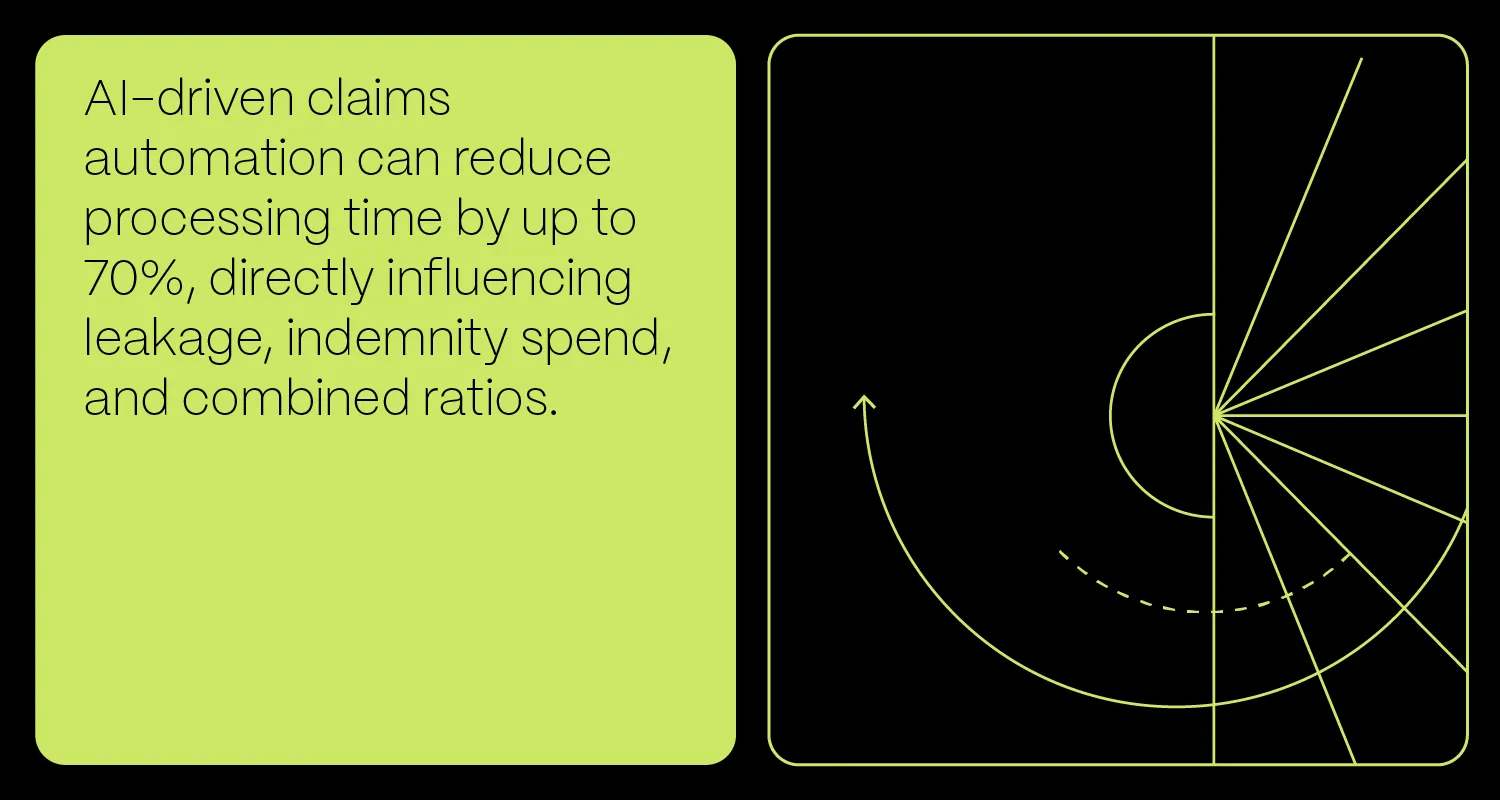

Claims performance has become one of the strongest arguments for large-scale AI adoption. McKinsey’s research shows that AI-driven claims automation can reduce processing time by 50 to 70%, directly influencing leakage, indemnity spend, and combined ratios. These improvements matter because they directly influence leakage, speed, and customer experience.

Additionally, KPMG’s industry research studies show that insurers such as Zurich Australia already use OCR, NLP, and machine learning to streamline document ingestion and route claims more accurately, reducing manual handoffs and improving downstream cycle times. Earlier detection of behavioural or financial anomalies, a capability highlighted in Swiss Re’s modelling work, further strengthens this advantage by enabling carriers to intervene before costs escalate.

That is why we can freely conclude that AI makes claims handling faster, more predictable, and more resilient. As inflation and complexity continue to rise, straight-through processing is becoming not just an efficiency lever but the foundation for sustainable claims economics.

As high-volume, low-premium risks grow and margins tighten, underwriting capacity is stretched thin. The result is delays, missed opportunities, and growing frustration on both sides. Clients are waiting longer for quotes, and underwriters are losing time they should spend on more complex risk assessments. That is where STP steps in, transforming how transactions are handled.

Read the entire article here2. Underwriting and pricing intelligence

Traditional, document-heavy workflows cannot keep pace with the complexity and speed required in today’s market. That is exactly why underwriting is moving toward a human-supervised, AI-enabled discipline where judgement is amplified by analytics, rather than constrained by legacy processes. And, research claims the same.

BCG’s research on personalised pricing shows that behavioural and contextual signals now play a central role in assessing risk. Yet, these patterns are too dynamic and granular for traditional actuarial models to interpret. AI fills this gap by analysing thousands of signals in real time, generating risk insights and pricing recommendations that underwriters would not be able to surface manually.

3. Fraud analytics and behavioural modelling

The combination of advanced analytics and real-time scoring is redefining how risk is understood, allowing organisations to respond with greater speed, precision, and resilience.

The aforementioned KPMG research includes a case study that demonstrates what this shift looks like in practice. A company uses AI-driven behavioural scoring to evaluate claims across millions of datapoints, enabling it to pay 95% of claims automatically while escalating only 5% for human review.

This level of automation is not merely a cost reduction mechanism. It reflects a bigger change in how fraud detection operates. Patterns are identified earlier, decision confidence increases, and frontline teams focus on complex or ambiguous cases rather than manual screening.

4. Document intelligence and large-scale ingestion

Many insurers still rely on manual extraction and spreadsheet-based processes, which makes it difficult to validate data, automate decisions, or scale AI across underwriting and claims. As long as critical information arrives in PDFs, scans, medical records, and free-text narratives, downstream processes will continue to inherit this fragmentation.

This is why document intelligence is becoming a foundational capability. Solutions, such as our Document AI accelerator, show what this looks like in practice.

Unstructured documents are processed automatically, data is extracted and validated with high accuracy, and outputs are delivered in a consistent format that downstream systems can use immediately. This eliminates manual bottlenecks and creates the reliable data layer that underwriting models, fraud engines, and claims workflows depend on.

Once the ingestion layer is automated, the rest of the value chain becomes faster, more predictable, and healthier from a risk perspective.

5. Customer experience and intelligent service automation

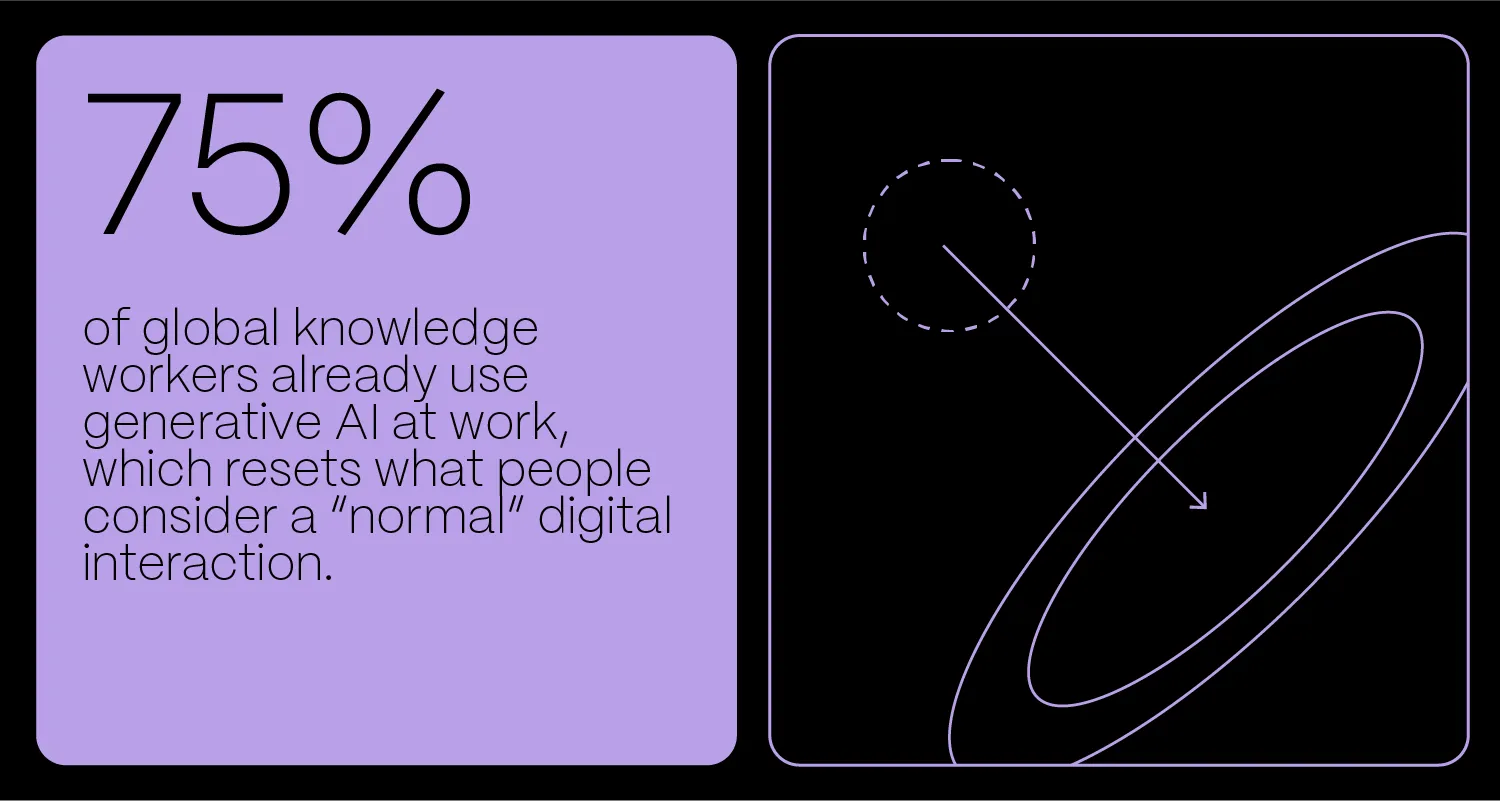

Microsoft and LinkedIn’s 2024 Work Trend Index shows that 75% of global knowledge workers already use generative AI at work, which resets what people consider a “normal” digital interaction. Customers now expect responses that are immediate, personalised, and context-aware.

This shift is pushing insurers to rearchitect their service layers, too. AI assistants, automated policy summarisation, and intelligent routing are becoming essential tools for reducing friction and delivering clarity at scale. They enable more precise pricing, coverage, and engagement at an individual or account level, driving higher conversion, retention, and lifetime value.

Who is gaining the most advantage

Insurers who built the data foundations AI depends on

The carriers moving ahead are those that treat data as infrastructure, not a by-product of operations.

KPMG’s maturity research shows that insurers with unified data platforms, cloud-based pipelines, and disciplined governance scale AI with fewer failures and greater reliability.

By eliminating fragmented inputs, these organisations enable underwriting, claims, and fraud models to operate on complete and consistent signals.

The advantage is immediate: faster deployment cycles, higher model accuracy, and a shared source of truth that elevates decision-making across the enterprise.

Insurers who place AI inside the decision flow, not on top of it

The strongest performers embed AI into the core of their workflows rather than layering it onto existing processes. Zurich Australia’s approach is a clear example: AI consolidates data and surfaces key risk indicators upfront, enabling underwriters to focus on judgement instead of document assembly.

This embedded architecture consistently differentiates high performers. When AI accelerates the first stage of assessment and human expertise refines the outcome, decisions become faster, more consistent, and structurally more accurate. This creates a compounding advantage that slower adopters struggle to replicate.

Insurers adopting enterprise-wide AI strategies

The insurers moving fastest are not those with the most AI pilots, but those with a unified AI strategy. KPMG reports that 47% of insurers experimenting with AI have established centres of excellence, compared with a 40% global average.

This is surely a signal that governance and alignment are becoming competitive differentiators.

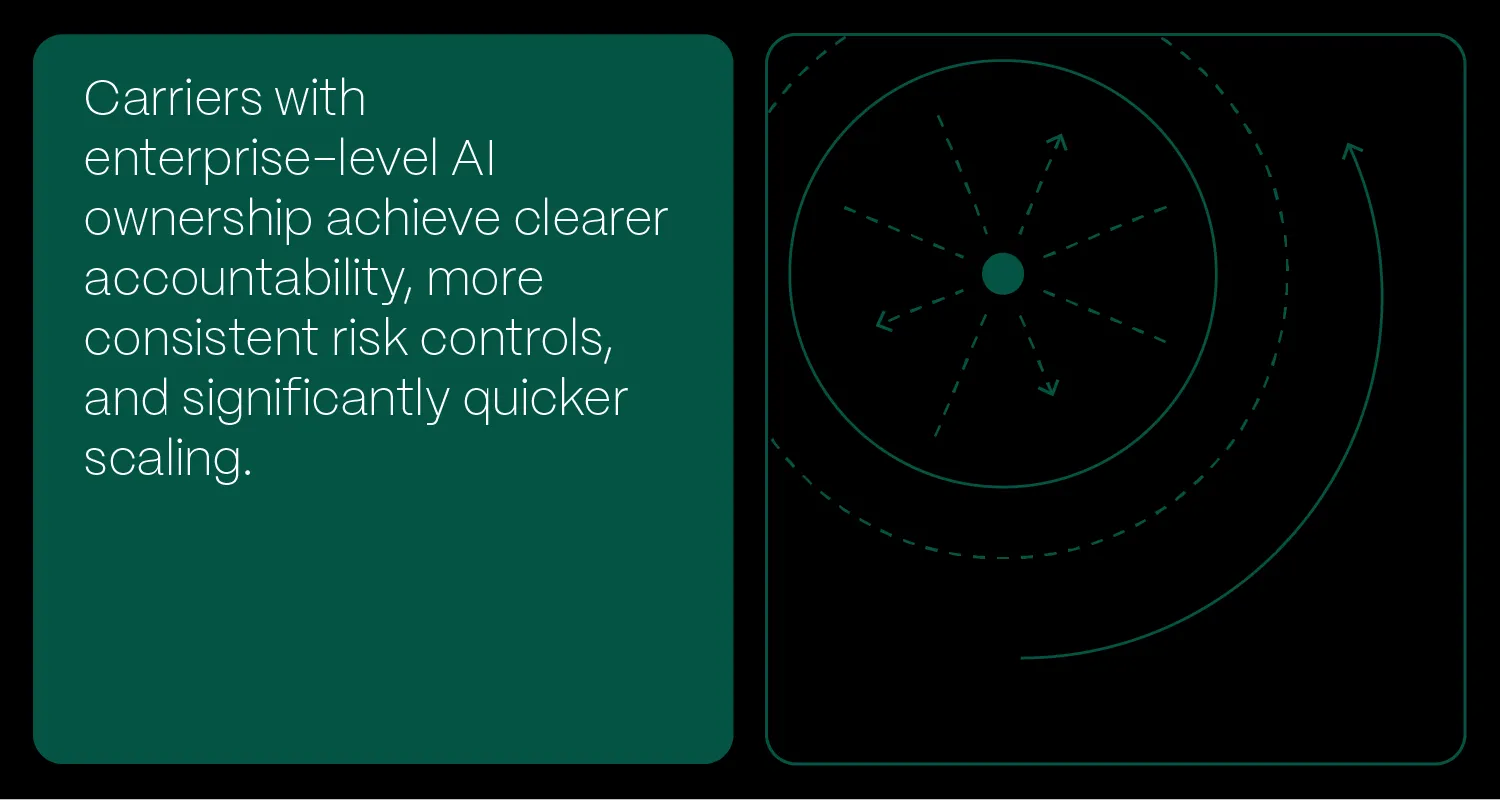

Deloitte’s outlook shows the impact of this approach: carriers with enterprise-level AI ownership achieve clearer accountability, more consistent risk controls, and significantly quicker scaling.

One North American multiline insurer, for instance, redesigned its AI operating model so pricing, underwriting, claims, and fraud teams share standards, data pipelines, and validation protocols. This reduced duplicated effort and cut model deployment times from months to weeks.

Key takeaways: Acting at the pace of the industry, not the pace of comfort

AI is reshaping every component of the insurance value chain faster than incremental transformation can keep up.

The insurers that lead will be those willing to rethink their operating model, strengthen their data foundations, and embed AI across core decision flows. The industry has entered a new phase. The question is no longer whether AI will define the next decade of insurance, but which organisations will have the discipline and scale to realise its full potential.